American taxpayers will experience major changes in the upcoming tax season as a result of President Donald Trump’s new tax cuts.

Trump has said this is expected to be the “largest tax refund season of all time,” with one of the most significant changes being the elimination of taxes on car loan interest under the One Big Beautiful Bill Act (OBBBA).

The Internal Revenue Service and the Department of the Treasury issued official guidance on Dec. 31, 2025, for the new car loan interest deduction, which could allow drivers to claim up to $10,000.

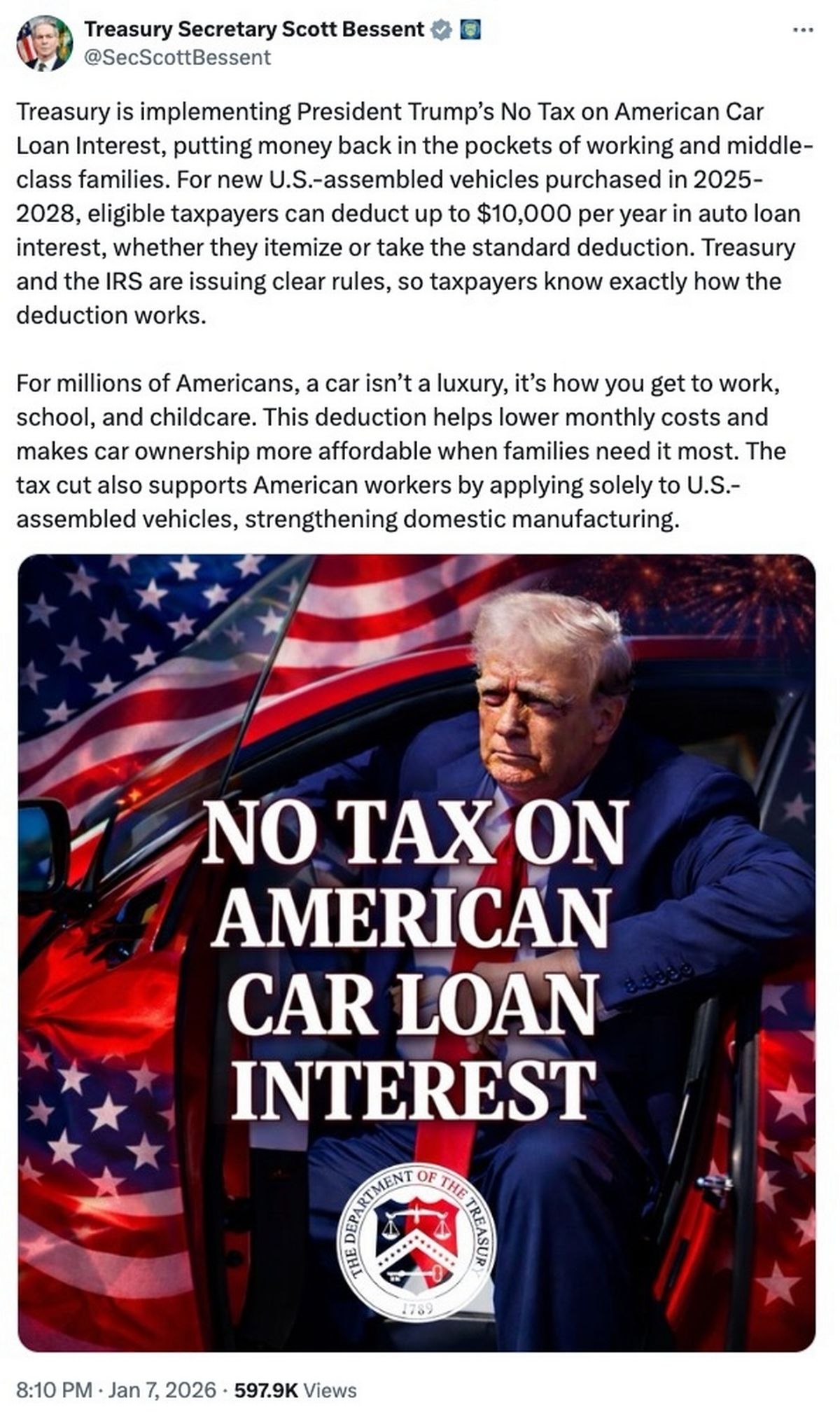

This deduction is expected to “[put] money back in the pockets of working and middle-class families,” Treasury Secretary Scott Bessent said on X on Wednesday, Jan. 7. “For new U.S.-assembled vehicles purchased between 2025 and 2028, eligible taxpayers can deduct up to $10,000 per year in auto loan interest, whether they itemize or take the standard deduction.”

“For millions of Americans, a car isn’t a luxury—it’s how you get to work, school, and childcare,” he added. “This deduction helps reduce monthly expenses and makes car ownership more affordable when families need it most.”

The auto loan interest tax cut applies only to new, made-in-America vehicles purchased for personal use after Dec. 31, 2024, and Bessent said the provision will support “American workers.”

Here’s everything you need to know about claiming Trump’s $10,000 auto loan interest tax cut:

Treasury Secretary

Scott Bessent touted the new auto loan tax deduction on X (Image: @SecScottBessent/X)

What is Trump’s car loan tax cut?

The auto loan interest tax cut was a central policy Trump promoted during his second-term presidential campaign.

“I will make interest on car loans fully tax deductible,” Trump said at a North Carolina rally in October 2024, according to Reuters. “I am only going to do it if they build that particular product — namely an automobile — in the United States.”

Under his megabill, the OBBBA, the president included a provision for “no tax on car loan interest,” along with other major policies such as no tax on tips, no tax on overtime, and a deduction for seniors. However, the legislation does not make vehicles fully tax deductible.

The new tax benefit applies to interest paid on car loans for vehicles purchased after Dec. 31, 2024, and the vehicle must be a “new made-in-America” model for personal use, according to the IRS.

Additionally, the IRS said in its guidance that “This new tax benefit applies to both taxpayers who take the standard deduction and those who itemize deductions.”

Am I eligible for Trump’s car loan tax cut?

Under the OBBBA, several requirements must be met to claim the auto loan interest deduction.

According to the IRS, the deduction applies only to qualified passenger vehicles — including cars, minivans, vans, SUVs, pick-up trucks, or motorcycles — with a gross vehicle weight rating under 14,000 pounds. The vehicles must also have completed final assembly in the United States.

The maximum annual deduction is $10,000, and the deduction decreases for high earners, phasing out for taxpayers with a modified adjusted gross income over $100,000, or $200,000 for joint filers.

Leave a Reply